Market

An attractive market

The global dermatology market size was USD 19.974 Billion in 2020 and is forecasted to reach USD 59.309 Billion in 2030 with a CAGR of 11.5% from 2021–2030. The future key drivers are believed to be psoriasis, dermatitis, acne, rosacea, alopecia and skin cancer.

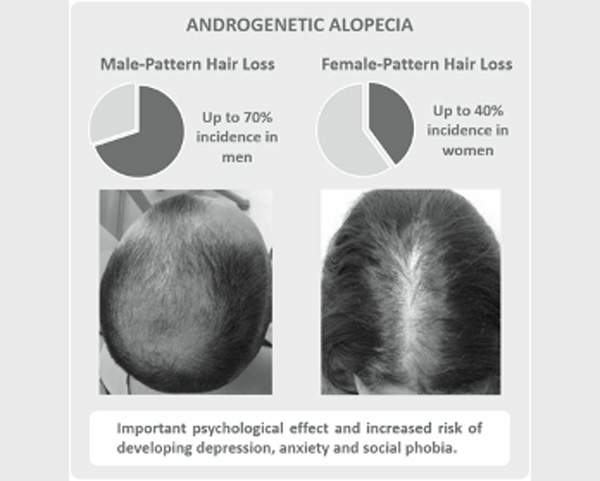

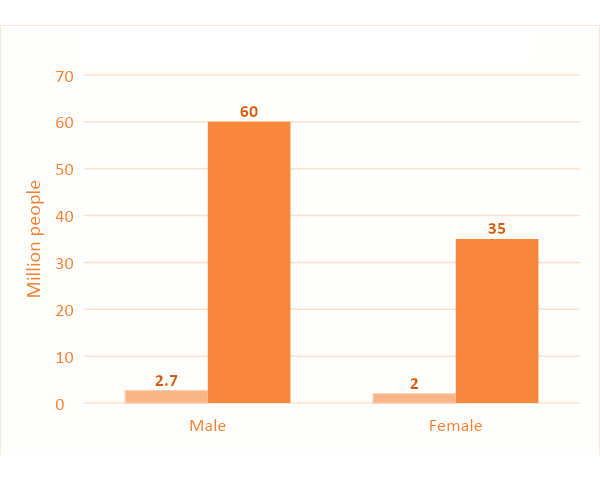

Alopecia, also known as hair loss or baldness, is a chronic dermatological disorder characterized by the partial or total loss of hair on the scalp. As there is a hormone and genetic element of the disease it is referred to as andro-genetic alopecia (AGA) and accounts for >95% of hair loss in men with 50–60 million men and 30–35 million women affected in the US alone. The incidence of AGA varies with ethnicity, but in general up to 70% of men and 40% of women experience some degree of AGA in their lifetime. Men usually suffer from hairline recession, while women typically develop a diffuse thinning over the top of the scalp (Fig. 1.A).

AGA is poorly understood but it is believed to be induced via activation of hormones or due to decreased vascularization of the hair follicles. More than 90% of patients are not being treated Figure 1.B

Reference: Allied Market Research, Dermatologicals market, Jan 2022, page 262

The global dermatology market is forecasted to reach USD 59.309 Billion in 2030

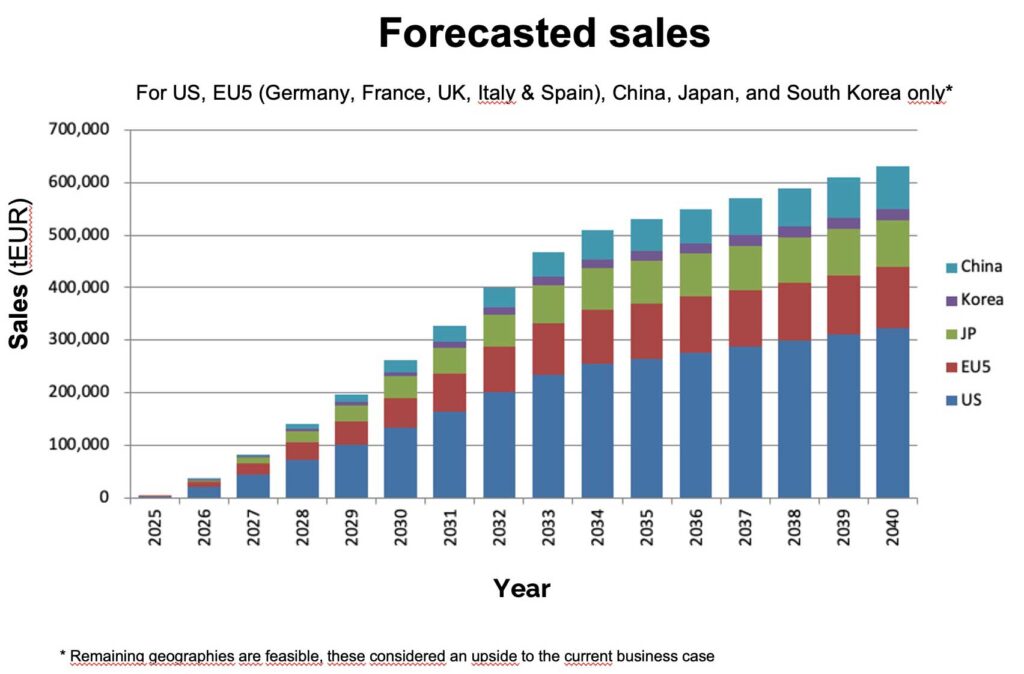

Projected annual peak sales reaching 600 mEUR in 2040

Existing treatments

FOL005-peptide gel benefits vs. hairloss drugs

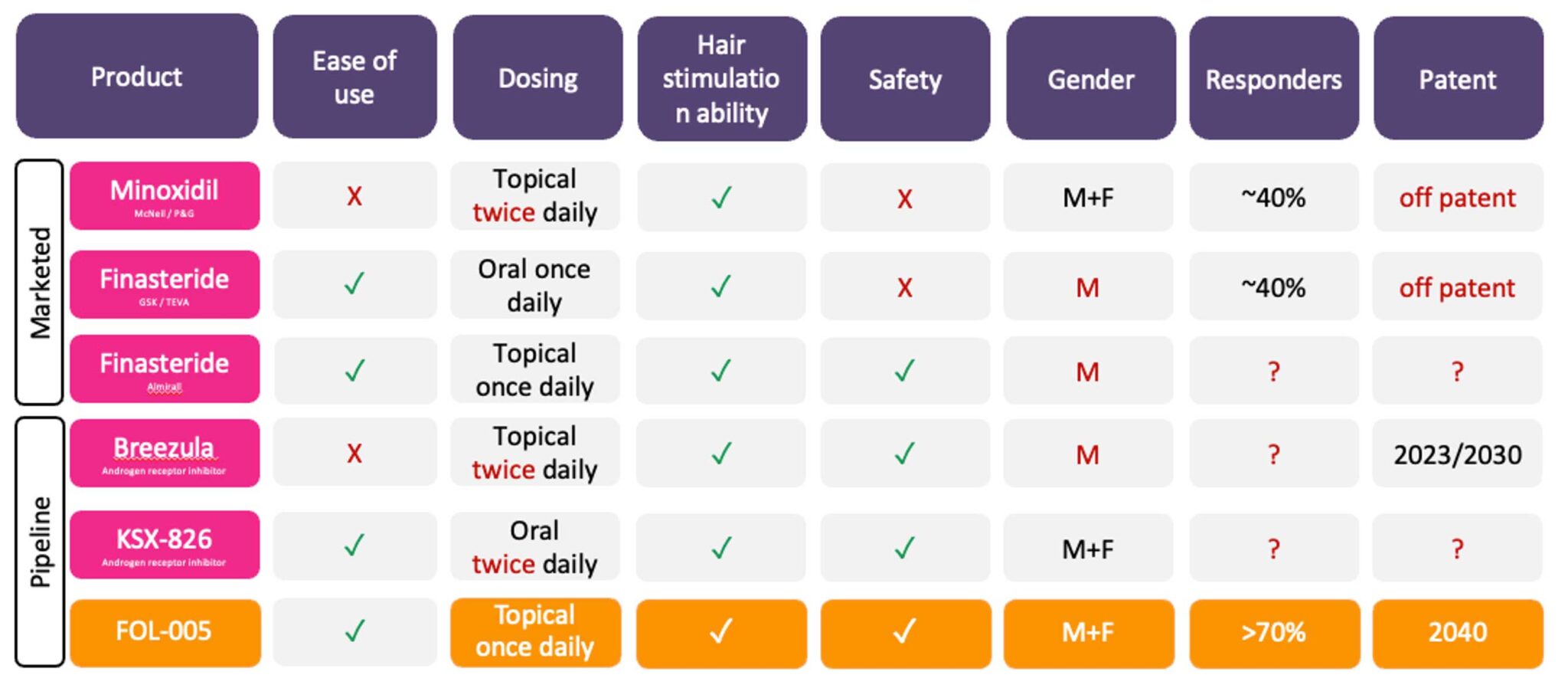

Currently, there are only two drug classes on the market to treat alopecia. However, these drugs have limited efficacy and response rate. In addition, they are associated with important side effects such as sexual function disorders or growth of hair in untargeted body parts. Therefore, there is a clear need for novel products to help people worldwide who suffer from alopecia to recover their hair and increase their quality of life. There are two EMA/FDA- approved drugs for the treatment of AGA, minoxidil and finasteride.

Minoxidil was initially developed by Upjohn Company (later part of Pfizer) in 1950 for the treatment of ulcers. After discovering its effect on hair growth, it was approved by the FDA in 1988 for the treatment of AGA. The exact mode-of-action (MoA) of minoxidil remains unknown, but it is reported to increase vascularization of the hair follicles. Minoxidil’s efficacy in the overall population remains relatively low, with approximately 30-40% of responders after one year. Common side effects of minoxidil include burning or irritation of the eye, itching, redness or irritation at the treated area, and unwanted hair growth elsewhere on the body.

Finasteride was developed by Merck & Co., patented in 1984, and approved by the FDA in 1997 for treatment of AGA. Finasteride is available only for men and it works by inhibiting the conversion of testosterone into DHT, the hormone that induces AGA. Regarding its efficacy, 50% of recipients experience improvements in hair growth at 1 year. Despite finasteride has a higher efficacy than minoxidil, it also has stronger side effects including sexual function disorders such as decreased libido and erectile dysfunction.

The response rate to treatment after one year is with minoxidil ~ 30–40% and finasteride 50%

Apart from minoxidil and finasteride, several drugs are prescribed off-label for the treatment of AGA. Among these we can find Dutasteride, which has a similar mode of action as finasteride. Other drugs under development might enter the alopecia market in the following years, including reformulation products of minoxidil or finasteride alone or in combination.

However, despite its huge potential, the alopecia market is characterized by slow developments due to the lack of funds obtained for research in the area, as alopecia is often seen as a cosmetic problem rather than a disease. Four products are in Phase 2/3 clinical trials at this moment, including Breezula by Cosmo Pharmaceuticals and KX-826 by Kintor Pharmaceutical.

Several non-pharmacological therapies exist such as hair transplantation, scalp reduction, stem cell transplantations and low-level laser therapy. Hair transplantation includes transplanting DHT-resistant follicles from other parts of the head to bald areas, while scalp reduction is an outdated procedure which entails stretching the hairy parts of the scalp to cover the parts that have no hair. In low-level laser therapy light photons are irradiated to the scalp and absorbed by cells to encourage hair growth. The main disadvantage of hair transplantations and scalp reduction is that these are temporal solutions which do not stimulate growth. Laser therapy is a time-consuming procedure that requires many sessions while the long-term safety and effectiveness is unclear.

Market size and Market for exits/out–licensing

Market size

The global market size is estimated in 2024 to be 3.2 bUSD for finasteride and 1.9 bUSD for minoxidil alone. There is a high unmet medical need with a large potential to expand the existing market as e.g. in the US alone only 4.5% men and 5.7% women are treated for AGA (Figure 1.B).

In conclusion, the current alopecia treatment market is characterized by few available medical products with moderate effect and safety concerns which leaves a high need for novel treatments with improved efficacy and safety profile. Existing cosmetic products are generally not well documented to stimulate hair growth.

The global market size is estimated to be 8 bUSD

Market for exits/out–licensing

We are seeking global and regional partners in the dermatology area for the launch, distribution and marketing of a safe proprietary product series which is clinically proven to stimulate hair growth. We are also seeking for maufacturing partners which can scale up the production of the peptide and finished goods at acceptable cost of goods.